Do you have mortgage questions? We have answers

Contact the Customer Service Department

Existing Home Loans

New Home Loans and Refinancing

Home Office Address

Need a Log-in?

If you do not currently have a log-in to the My Account section of GuildMortgage.com, and you want to access your loan information online, then please register for a log-in: https://myaccount.guildmortgage.com/guild-home/my-account/login/Already have a Log-in?

If you already have a log-in to the My Account section, and you want to manage an additional loan using the same log-in, then:- Log in to your account. Log-in here.

- Click on the “Attach a Loan” option in the sub-navigation.

- Type in your 10-digit loan number in the “Add a Guild loan to your account” field.

- Click the yellow “Save Changes” button at the bottom of the screen.

- When the screen reloads, there should either be a bright green message declaring success, or a bright red error message with further instructions!

Property Tax Information

If you have an escrow account for taxes, you do not need to forward a copy of your regular tax bill to Guild Mortgage Company. If you received an adjusted or corrected tax bill, you may fax the bill to 858-492-5835 or mail it to the address below. Please note that we must receive the tax bill ten (10) business days prior to the delinquent date. If we are not given sufficient time to pay your corrected or adjusted tax bill, any penalty will be charged to your escrow account.An escrow account (also referred to as impound or trust account) is an account for paying your property taxes and insurance premiums and for any other charges.

An estimated amount, based on the previous year’s payments and an adjustment for inflation, is divided by 12 and added to your mortgage payment.

Your monthly escrow payment could change. If your property tax payment or insurance premiums change then your escrow payment will also change.

An escrow cushion (also referred to as a reserve or target balance) is collected to cover any unanticipated disbursements or payment increases. The cushion amount may be 0-2 months of escrow payments based on federal and state guidelines and your loan documents.

An escrow analysis is a review of the escrow deposits and expenses for the previous year and the projected activity for the next year. Your account is analyzed yearly to make sure the correct amount is collected to cover your property taxes and insurance premiums, and the cushion. Watch our video for details on how to read your escrow statement.

An escrow analysis is conducted to project deposits and expenses for the next 12 months. If at any time your projected escrow balance is less than the allowable cushion then a shortage will exist. If at any time the projected escrow balance is greater than the allowable cushion then a surplus will exist.

If a shortage exists, the shortage amount is typically spread over 12 months and is added to the projected monthly escrow payment. If you choose to pay off the total shortage your monthly payment could still increase due to increases in taxes and insurance premiums.

If you have a surplus less than $50.00 the surplus will remain in your escrow account and will be used to decrease your monthly escrow payment. If the surplus is equal to or greater than $50.00 then you will receive a refund check unless your loan is delinquent. In that case, you will be asked to contact Loan Counseling to discuss ways of handling the surplus.

By law, a small reserve (also called a cushion) may be collected to cover any unexpected changes in escrow payments. The cushion may be 0-2 months of escrow payments.

According to RESPA guidelines, a surplus equal to or greater than $50.00 shall be refunded to the borrower.

If you have set up automatic payments through ACH, then the amount taken from your account will be adjusted to cover any decrease or increase starting on the effective date of the new payment. If you have set up automatic payments through your financial institution’s bill pay service, you will have to adjust future payments to the new amount due.

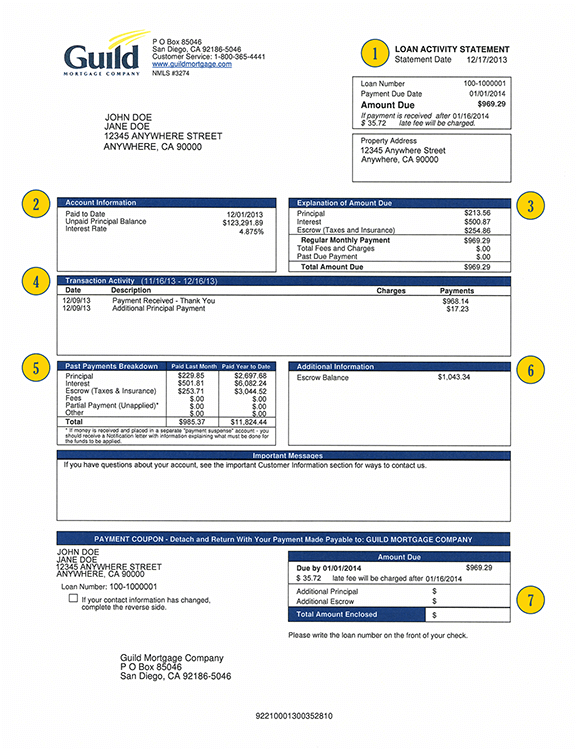

STATEMENT DATE | The date your statement is printed. Any payments or transaction activity after this date will not be shown.

Your Paid To Date is the date your loan’s interest is paid through. The Unpaid Principal Balance is the unpaid portion of the loan amount (this does not include interest). If your loan has been modified with a deferred principal balance, it will include the non-interest bearing deferred principal. If so, you will see the amount of deferred principal in the Additional Information box. The Interest Rate is the rate of interest charged on your loan. If your loan is an adjustable rate mortgage or a modified loan that will step up to a new interest rate, the next interest rate change date will be listed here.

This section includes payment information for the next scheduled Regular Monthly Payment and any past due fees and payments. Your Regular Monthly Payment is broken down to show how it will be allocated toward principal, interest, and escrow items. Any Fees and Charges such as previously assessed late fees or Non-Sufficient Funds (“NSF”) charges that remain unpaid and any past due payments are all included in the total Amount Due. Your Escrow includes the monthly amount currently due for the payment of taxes, insurance and Optional Personal Insurance, if applicable.

This section includes all transaction activity since your last Loan Activity Statement including any fees accessed. You will see disbursements made on your behalf from your escrow account as a negative number in the payments column and any payment received from you as a positive number.

This section includes the total of all payments received since your last Loan Activity Statement and how it was applied to principal, interest, escrow, fees and unapplied account, if applicable (Paid Last Month column). Also included is the total of all payments received since the beginning of the calendar year and the corresponding application to principal, interest, escrow, fees and the balance currently in unapplied, if applicable (Paid Year to Date column).

Your Escrow Balance is the current balance of your escrow account after any disbursements made on your behalf and any deposits made into your account.

You may elect to include extra money towards principal and extra money towards your escrow account. ACH Customers: With this Loan Activity Statement format beginning January 2014, we have turned paper statements back on. You may still opt out of receiving paper statements. To opt out after making sure you can view your statement on line go to the Account Settings.

What fees are associated with servicing my loan?

The schedule below lists common fees that could be associated with servicing a loan. This is not a complete list and is to be used for informational purposes only.Common Servicing Fees

This fee schedule is provided for informational purposes. It outlines typical fees that could be assessed for servicing a mortgage loan.| Fee | Fee Amount | Fee Description |

| Assumption | $300-$1,800 | Fee charged upon completion of changing the individual(s) legally responsible for repaying a loan. |

| Reconveyance | $0.00 | Fee for services required to release (reconvey) a lien. The fee is calculated according to the Deed of Trust or Mortgage. |

| Recording | Varies | A government fee assessed for legally recording the Deed of Trust or Mortgage and other documents related to the loan. The fee is determined by the county. |

| Tax Penalties | Varies | Any fees assessed, by the county, for delinquent taxes that are the borrower’s responsibility. |

| Late Charge | Varies | Fee for payment received after the 16th of the month. The fee is as determined on the Note and is based on the amount past due. |

| Non-Sufficient Funds | $15 | Fee for processing and/or reprocessing checks returned as uncollectable. Maximum as allowed by the state. |

| Speedpay | Varies | The fee charged for making payment using any method through Speedpay, including automated phone payments, representative assisted payments and Guild website payments. Fee varies by state up to $7.00. |

| Foreclosure | Varies | Fees associated with the foreclosure process. Those fees may include, but are not limited to, attorney services, publication costs and title report and searches. |